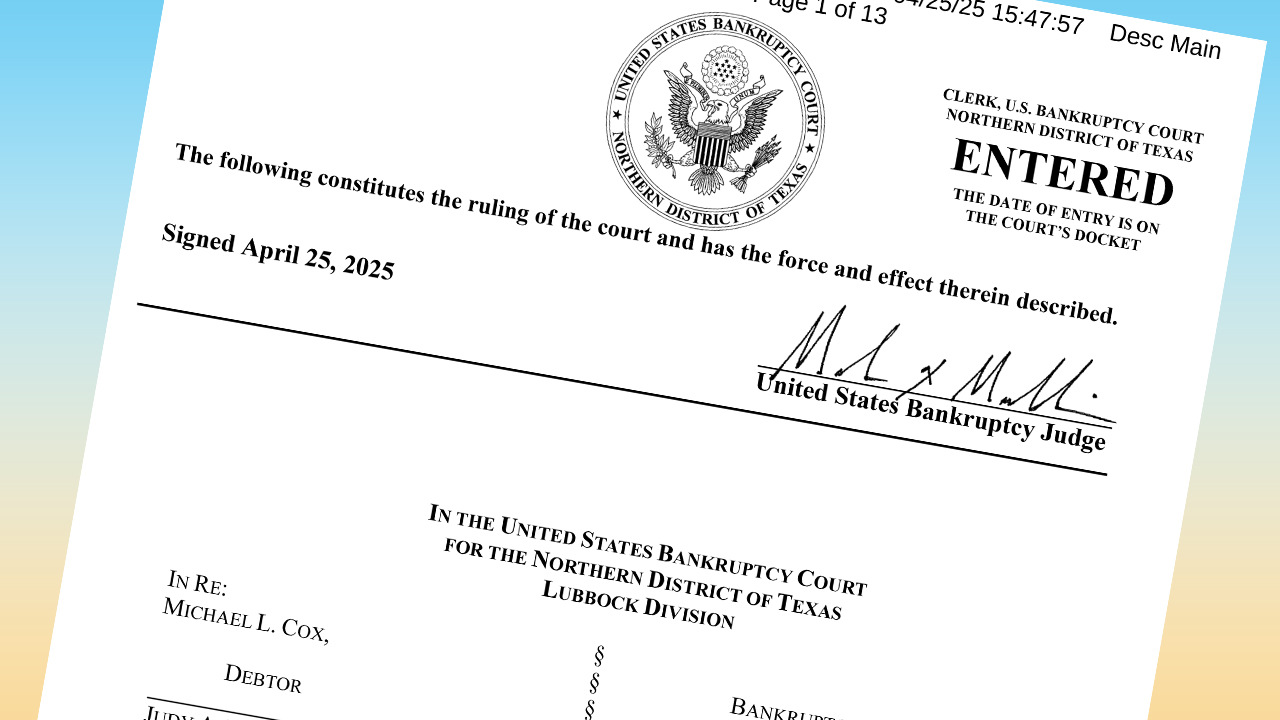

A Fort Worth bankruptcy judge ruled late Friday afternoon Mike Cox cannot discharge $21.7 million of his debt because Lubbock-based Ferrum Capital illegally sold unregistered securities. The judge’s ruling directly affects 66 people or couples who jointly filed an objection to the bankruptcy.

The larger bankruptcy case involved nearly 400 people or businesses and more than $82 million as of our March 4 report on LubbockLights.com.

The case came to light in December when federal prosecutors announced criminal charges against Brooklynn Chander Willy, a radio host and financial advisor in San Antonio. Willy was charged with obstruction of an FBI investigation in Lubbock and San Antonio, wire fraud, securities fraud and more.

Willy’s criminal case remains pending.

Court records, including several lawsuits across the state, tied Willy to Ferrum and her own company, Queen B Advisors, LLC. Bankruptcy records also tied Cox to Ferrum so-much-so that most of his debt was related to Ferrum.

Judge Mark X. Mullin ruled Cox is liable as a “control person” under Texas law – meaning he owned or had actual power over Ferrum. Official state records indicated he was half-owner and an officer of the company.

The judge also mentioned MLC Financial, Inc., Allen Financial and Joshua Allen as having control over the sale of financial products by Ferrum.

Ongoing coverage of Ferrum Capital

-

- Hundreds may have lost millions with troubled local company after criminal case extends to Lubbock from San Antonio

- More charges filed in San Antonio related to FBI investigation of troubled Lubbock firm; one victim speaks about losing retirement savings

- Deal proposed in Lubbock $82 million Mike Cox bankruptcy case could recover small portion for Ferrum participants

- Threat illustrates frustration of Ferrum Capital investors, who want to know where money went, if they’ll recover any

- Cox bankruptcy case in Lubbock may get new judge, as hundreds wait to see about their millions of lost savings

Cox tried to argue he did not know Ferrum’s activity would be considered the sale of unregistered securities. The judge disagreed.

Cox tried to argue Ferrum did not sell unregistered securities but instead people were loaning money to Ferrum. Ferrum, according to a series of lawsuits, turned over the money to Collins Asset Group. Collins would then use the money to purchase distressed debt for pennies on the dollar and make money if the debts could be recovered.

Ferrum defaulted in 2023. Cox filed for bankruptcy not long after.

Certain kinds of debt are, by definition, securities and must be properly registered with either state or federal officials.

But the judge took it further than that.

“The Ferrum Entities were operated as a Ponzi scheme in that new investor money and funds pledged to other investors were used to pay early investors,” the ruling said.

“[Cox] owes a debt to plaintiffs that arises from violations of Texas securities laws … [Cox’s] debts to plaintiffs are nondischargeable … because the debts are for a violation of state or federal securities law,” the ruling continued.

The bankruptcy trustee, just two days before the ruling, issued a report showing Cox had just under $2 million in assets.

Allen was featured prominently in the ruling and in other court cases since Ferrum defaulted. At last check, Allen had not filed for bankruptcy. Neither Allen nor Cox have been charged with a crime.

LubbockLights.com reached out to attorneys for Cox and Allen on several occasions since our coverage began in December. If either wants to comment, we will provide updates.

LubbockLights.com also reached out to several attorneys in the case late Friday. If appropriate, this story will be updated.

Please click here to support Lubbock Lights.

Comment, react or share on our Facebook post.

Facebook

Facebook